Malaysia Income Tax Act : Impacts Of The Self Assessment System For Corporate Taxpayers - Any services rendered at any time in the course of carrying on a business;.

Malaysia Income Tax Act : Impacts Of The Self Assessment System For Corporate Taxpayers - Any services rendered at any time in the course of carrying on a business;.. Allowance under schedule 2 or schedule 3 of the income tax act 1967 has been claimed on the expenditure. You'll still need to pay taxes for income earned in malaysia and will be taxed at a different rate from residents. Laws of malaysia act 543 petroleum (income tax) act 1967 arrangement of sections p art i preliminary section 1. (1) the minister may make rules— (c) implementing or facilitating the operation of an arrangement having effect under section 132, 132a or 132b; This is because that income is not derived from the exercising of employment in malaysia.

Rujukan kepada akta cukai pendapatan 1967 yang mengandungi pindaan terkini yang dibuat oleh akta kewangan 2017 akta 785 boleh diakses melalui portal rasmi jabatan peguam negara di pautan berikut: Foreign income remitted into malaysia is exempted from tax. The income of a resident individual is subject to income tax at progressive rates after personal relief while the income. Interpretation part ii imposition and general characteristics of the tax 3. It is trite law that double tax agreement (dta) is not a taxing statute and therefore, if an income or profit arising from a particular transaction or

Income Tax Act 1967 Pustaka Mukmin Kl Malaysia S Online Bookstore from cdn.store-assets.com Section 3 income tax act, 1967 (ita) says that income shall be charged for the income of any person accruing in or derived from malaysia or received in or from malaysia. the phrase accrues in or from malaysia tells to that the income source should be from malaysia. Laws of malaysia act 53 income tax act 1967 an act for the imposition of income tax. On the first 5,000 next 15,000. The income tax act 1967 (malay: (1) the minister may make rules— (c) implementing or facilitating the operation of an arrangement having effect under section 132, 132a or 132b; Generally, income taxable under the income tax act 1967 (ita 1967) is income derived from malaysia such as business or employment income. You'll still need to pay taxes for income earned in malaysia and will be taxed at a different rate from residents. Interpretation p art ii imposition of the tax 3.

The new guidelines are broadly similar to the earlier guidelines and explain the penalties that will be imposed under section 112(3) of the income tax act 1967 (ita), section 51(3) of the petroleum (income tax) act 1967 (pita) and section 29(3) of the real property gains tax act 1976 (rpgta) where a taxpayer fails to furnish a tax return within.

(3) this act shall have effect for the year of assessment 1968 and subsequent years of assessment. Laws of malaysia act 543 petroleum (income tax) act 1967 arrangement of sections p art i preliminary section 1. Review of corporate income tax rate for small and medium enterprise (sme) it is proposed that the income tax rate on first rm500,000 of chargeable income of sme be reduced from 18% to 17%. Interpretation p art ii imposition of the tax 3. Income tax is imposed on a territorial basis. Any services rendered at any time in the course of carrying on a business;. Charge of petroleum income tax 4. It is trite law that double tax agreement (dta) is not a taxing statute and therefore, if an income or profit arising from a particular transaction or You'll still need to pay taxes for income earned in malaysia and will be taxed at a different rate from residents. The new guidelines are broadly similar to the earlier guidelines and explain the penalties that will be imposed under section 112(3) of the income tax act 1967 (ita), section 51(3) of the petroleum (income tax) act 1967 (pita) and section 29(3) of the real property gains tax act 1976 (rpgta) where a taxpayer fails to furnish a tax return within. Types of taxable compensation what categories are subject to income tax in general situations? Generally, income taxable under the income tax act 1967 (ita 1967) is income derived from malaysia such as business or employment income. Allowance under schedule 2 or schedule 3 of the income tax act 1967 has been claimed on the expenditure.

Excerpt of s154(1)(c), s132, s132a and s132b of the income tax act 1967 (laws of malaysia act 53) power to make rules 154. Laws of malaysia act 543 petroleum (income tax) act 1967 arrangement of sections p art i preliminary section 1. Malaysia income tax act 1967 up to january 1, 2006 this document was downloaded from asean briefing (www.aseanbriefing.com) and was compiled by the tax experts at dezan shira & associates (www.dezshira.com).dezan shira & associates is a specialist foreign direct investment practice, providing corporate Manner in which chargeable income is to be ascertained p art iii ascertainment of chargeable income Charge of petroleum income tax 4.

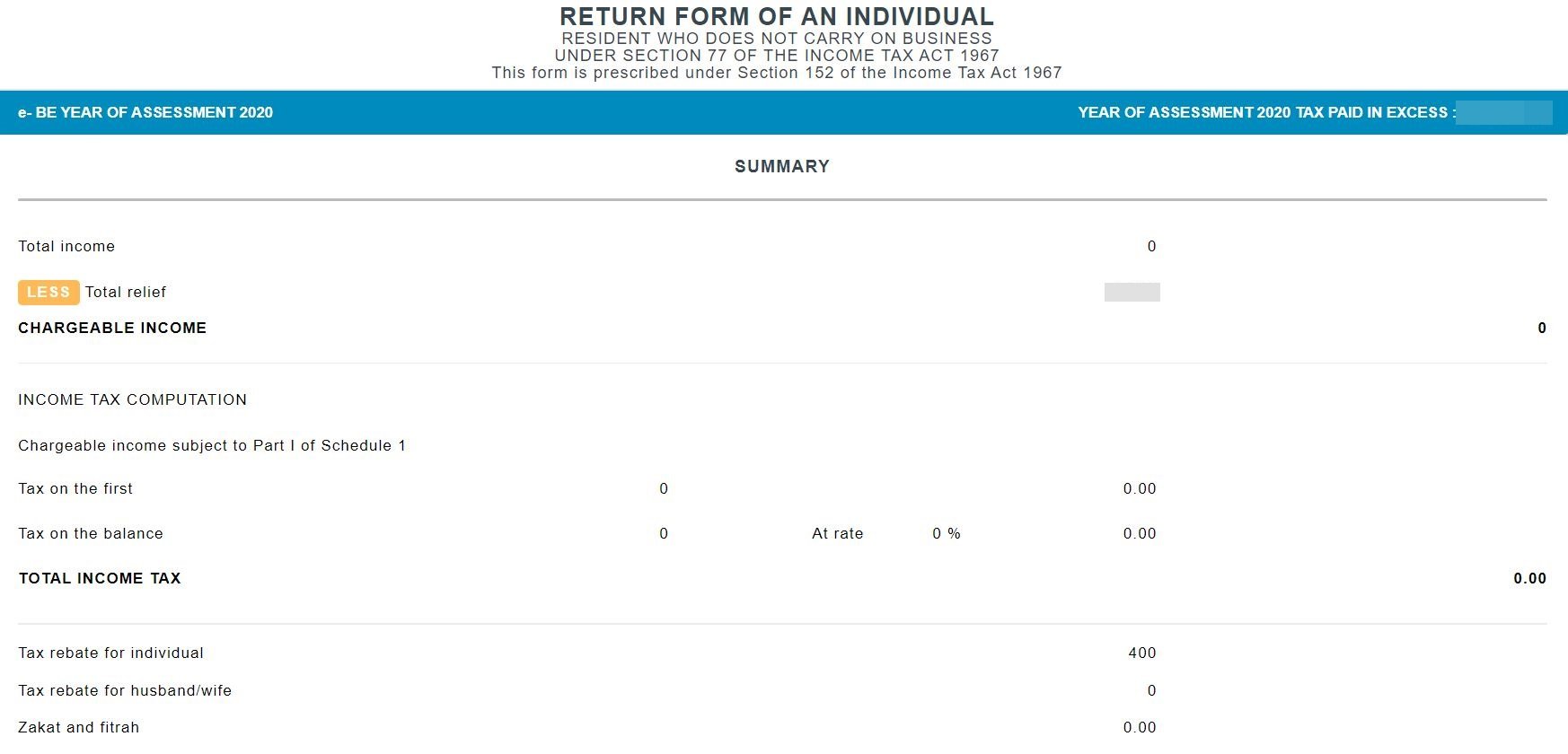

Malaysia Personal Income Tax Guide 2021 Ya 2020 from ringgitplus.com (3) this act shall have effect for the year of assessment 1968 and subsequent years of assessment. Utama / akta cukai pendapatan 1967. An approved ohq company is eligible for income tax exemption for a period of 10 years under section 127 income tax act 1967 for income derived from the following sources. Section 127 of income tax act 1967. It is trite law that double tax agreement (dta) is not a taxing statute and therefore, if an income or profit arising from a particular transaction or Excerpt of s154(1)(c), s132, s132a and s132b of the income tax act 1967 (laws of malaysia act 53) power to make rules 154. The income of a resident individual is subject to income tax at progressive rates after personal relief while the income. Types of taxable compensation what categories are subject to income tax in general situations?

Short title and commencement 2.

Laws of malaysia act 53 income tax act 1967 an act for the imposition of income tax. Short title, extent and commencement 2. Income tax act 1967 (online version as at 1 january 2019) (copy) hit(s) : (3) this act shall have effect for the year of assessment 1968 and subsequent years of assessment. Widening of scope of withholding tax (wht) under the income tax act 1967 as follows: This is because that income is not derived from the exercising of employment in malaysia. This volume contains the full text of the income tax act 1967. An approved ohq company is eligible for income tax exemption for a period of 10 years under section 127 income tax act 1967 for income derived from the following sources. Short title and commencement 2. Malaysia is chargeable to tax in malaysia regardless of whether the se rvices are performed in or outside malaysia. You'll still need to pay taxes for income earned in malaysia and will be taxed at a different rate from residents. Foreign income remitted into malaysia is exempted from tax. On the first 5,000 next 15,000.

With effect from ya 2004, foreign source income derived from sources outside malaysia and received in. It is trite law that double tax agreement (dta) is not a taxing statute and therefore, if an income or profit arising from a particular transaction or Charge of petroleum income tax 4. Income tax is imposed on a territorial basis. Therefore, income received from employment exercised in singapore is not liable to tax in malaysia.

Pdf Complexity Of The Malaysian Income Tax Act 1967 Readability Assessment Semantic Scholar from d3i71xaburhd42.cloudfront.net (3) this act shall have effect for the year of assessment 1968 and subsequent years of assessment. It is trite law that double tax agreement (dta) is not a taxing statute and therefore, if an income or profit arising from a particular transaction or Restriction on deductibility of interest section 140c, income tax act 1967 study group on asian tax administration and research(sgatar) commonwealth association of tax administrators(cata) Malaysian income tax act, 1967 (mita). Widening of scope of withholding tax (wht) under the income tax act 1967 as follows: Section 127 of income tax act 1967. Interpretation p art ii imposition of the tax 3. Foreign income remitted into malaysia is exempted from tax.

Generally, income taxable under the income tax act 1967 (ita 1967) is income derived from malaysia such as business or employment income.

On the first 5,000 next 15,000. Laws of malaysia act 53 income tax act 1967 an act for the imposition of income tax. Interpretation part ii imposition and general characteristics of the tax 3. An approved ohq company is eligible for income tax exemption for a period of 10 years under section 127 income tax act 1967 for income derived from the following sources. Akta cukai pendapatan 1967), is a malaysian law establishing the imposition of income tax. Allowance under schedule 2 or schedule 3 of the income tax act 1967 has been claimed on the expenditure. Rujukan kepada akta cukai pendapatan 1967 yang mengandungi pindaan terkini yang dibuat oleh akta kewangan 2017 akta 785 boleh diakses melalui portal rasmi jabatan peguam negara di pautan berikut: Income tax is imposed on a territorial basis. (1) the minister may make rules— (c) implementing or facilitating the operation of an arrangement having effect under section 132, 132a or 132b; The income of a resident individual is subject to income tax at progressive rates after personal relief while the income. Charge of income tax 3 a. Types of taxable compensation what categories are subject to income tax in general situations? Section 3 income tax act, 1967 (ita) says that income shall be charged for the income of any person accruing in or derived from malaysia or received in or from malaysia. the phrase accrues in or from malaysia tells to that the income source should be from malaysia.

Related : Malaysia Income Tax Act : Impacts Of The Self Assessment System For Corporate Taxpayers - Any services rendered at any time in the course of carrying on a business;..